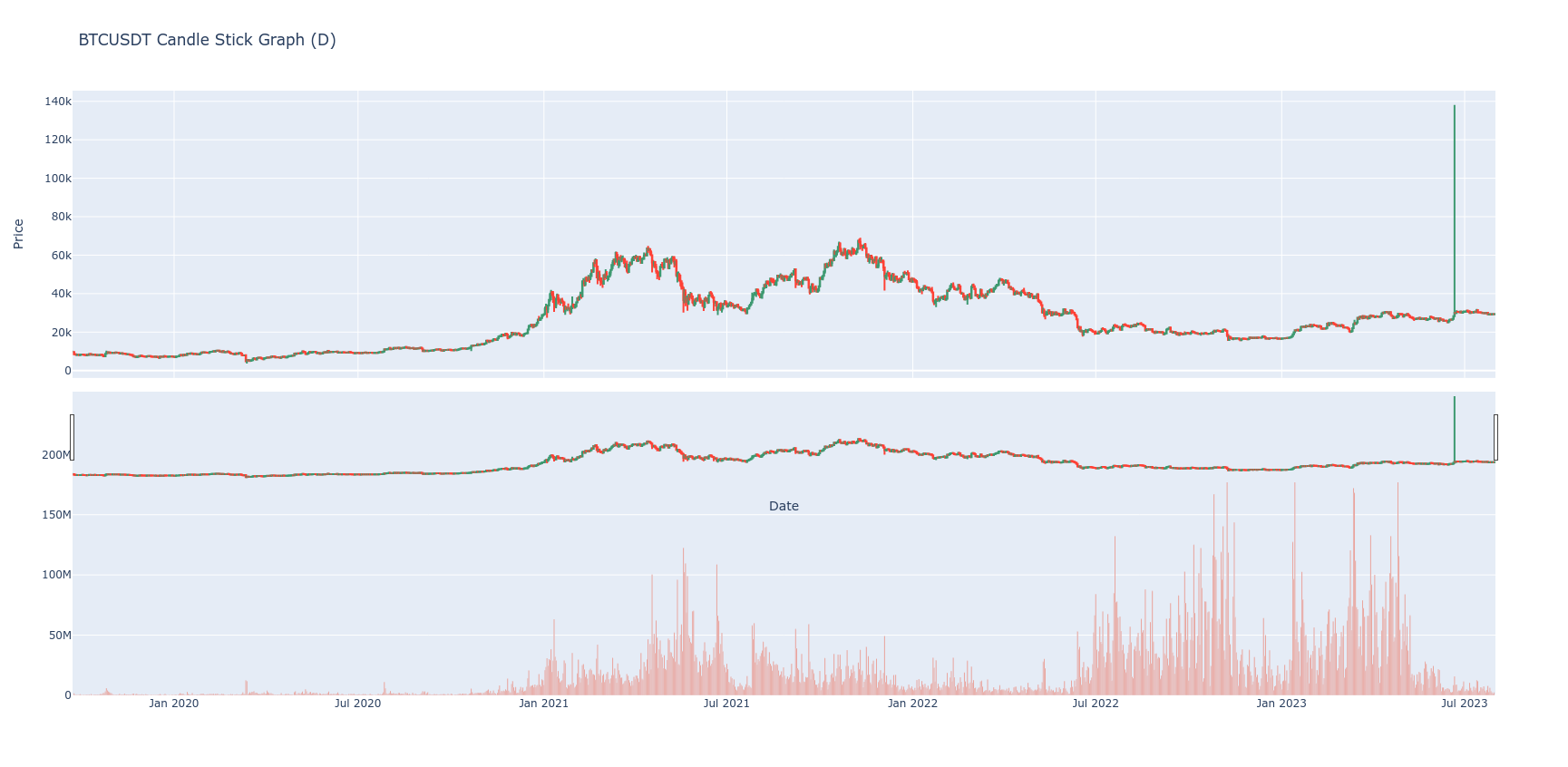

Bitcoin is a decentralized digital currency and the first-ever cryptocurrency created in 2009. Analyzing cryptocurrency pricing data is going to be of high interest to the Fintech community. Getting access to this price data is readily available through both graphs and numerical datasets. The sources that are available make it incredibly difficult to get OHLC and volume data at fine-grained resolution below 1-min intervals. When simulating financial models, fine-grained datasets can significantly impact model effectiveness. Our research aimed to extract cryptocurrency time-series data from the largest cryptocurrency exchange in the world, Binance. However, obtaining high-quality, one-second granularity data from exchange APIs and even online websites proved difficult, unintuitive, impossible, or expensive. This challenge inspired us to create an efficient Python-based framework that extracts the transaction history for 153 cryptocurrency trading pairs from Binance.us since September 2019. This data is then cleaned and summarized into a variety of sub-datasets ranging from yearly to one-second granularity candlesticks. To enable ease of data-sharing, we published a sample (4-year BTC-USDT trading pair data) dataset on Kaggle and the entirety of the 261GB datasets in CSV formatted files on a publicly accessible web server that updates nightly.